We use cookies to improve your experience on our website. By continuing you acknowledge cookies are being used.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

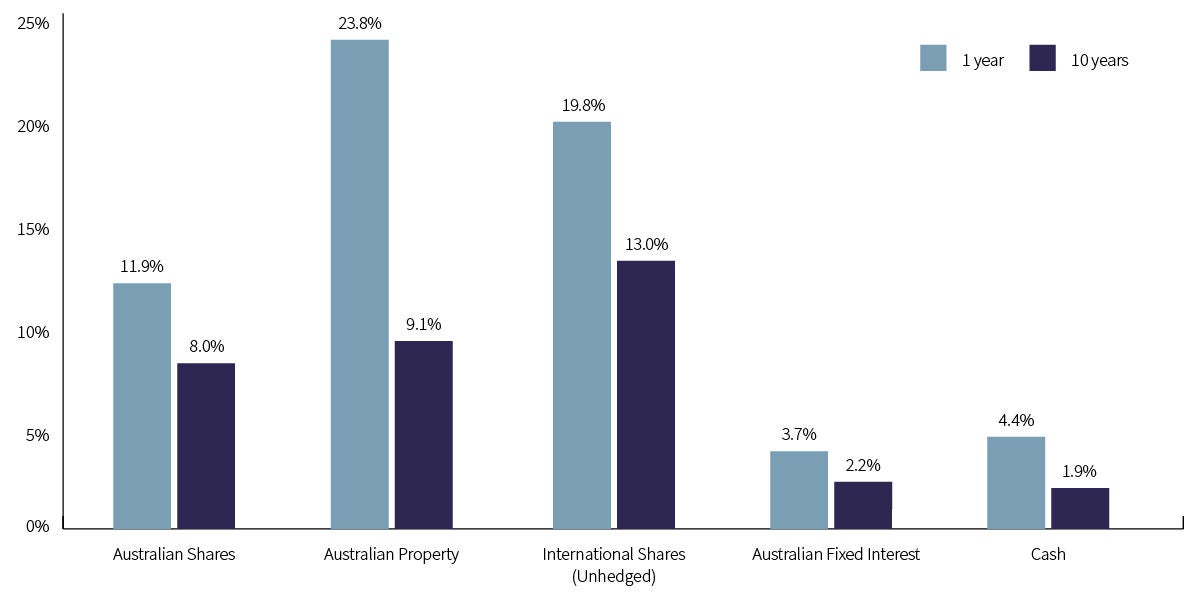

| Australian shares | -1.3 | 11.9 | 8.0 |

The Australian market began the quarter on a weak note with valuations taking a step back after the strong rally through Q4 2023 and Q1 2024. April saw inflation reignite concerns with investors again as the US and Australia experiencing inflation stabilizing above their target levels and expectation for the number of rate cuts in 2024 reduced significantly. Australia took its lead from the US markets as investors accepted the higher for longer expectations for interest rates and AI and Technology drove the US market higher.

The Australian market recouped more than half the April losses with the with the broad market index, the S&P/ASX 300 Accumulation Index only losing -1.2% over the quarter. Australian equities lagged their US counterparts as our exposure to AI and technology companies is significantly smaller. The best performing sectors were Utilities (+13.3%), benefiting from EVs and Data Centres driving demand for electricity. Financials and Information Technology also performed well up +4.0% and 2.4% respectively. The worst performing sectors for the quarter by was Energy (-6.7%) and Materials (-5.9%).

From a market capitalisation perspective, small caps reverse Q1 2024 strong returns, declining -4.5% Large Caps outperformed lead by good performance select banking companies. Micro caps surprised only easing -0.5% outperforming the broader equity market for the quarter.

At a style level, Value outperformed in April but quickly gave back its lead as Growth and Momentum rebounded to outperform the broader market over the quarter.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

| Australian shares | -1.3 | 11.9 | 8.0 |

The S&P/ASX 300 A-REIT Accumulation Index had retreated significantly in April as concerns that inflation was rearing its ugly head weighed on the interest rate sensitive sector. April’s declines weighed on the performance over the quarter, but the financial year returns remain robust. Goodman Group (+3.2%) stood out again over the quarter, benefiting from its exposure to data centres.

Australian Inflation has been stubbornly robust over the quarter, and the RBA has considered the potential of an interest rate increase. Even if the RBA keeps rates steady, the tailwind from interest rate expectations that helped drive some of the recent price gains are expected to ease over the near term

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

| Australian listed property trusts | -5.7 | 23.8 | 9.1 |

International markets consolidated after a strong Q4 2023 and Q1 2024. On a currency unhedged basis, international shares edged up by 0.3%. During this quarter, the AUD provided a small headwind to overseas returns, as the AUD appreciated by around 2.4% against the U.S. dollar and 3.2% against the Euro.

From a style level, Value outperformed in April but quickly gave back its lead as Growth, Momentum and Quality rebounded to outperform the broader market over the quarter. Global small caps were hurt during the risk off month of April but also lagged during the rebound in May and June as large companies were more exposed to AI and Technology leaders.

In the U.S., April saw a quick market reversal as concerns that inflation may not be processing downward at a sufficient pace. The US Federal Reserve rules out an increase in rates fairly quickly but re-iterated a higher for longer stance as the US Labour market and Consumer remained resilient. May saw investors buy the dip especially in the sectors and companies du jour of AI and its related technology beneficiaries.

The Chinese Sharemarket also showed signs of life over the quarter as the Chinese government began to issue its 1 trillion yuan (AU$204 bln) debt package which will be used to support the ailing economy and try to offset the headwinds of their ongoing property crisis.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

International shares | 0.3 | 19.8 | 13 |

The June quarter produced small negative returns as inflation and interest rate expectations received a jolt in April, which saw yields jump and bond prices decline. The main Australian Fixed Interest index, the Bloomberg AusBond Composite 0+ Years Index eased by -0.8% for the quarter.

Australian yields increased over the quarter, with the short end (2-year) of the curve rising by 0.48%. At the long end of the curve, the 10-year yield rose by 0.3.4%.

The yield to maturity at the quarter’s end was approx. 4.5% for Australian Bonds, with the index having around 5.8 years duration. This makes most mainstream Australian Fixed Interest funds a strong foundation for the defensive income producing portion of portfolios. The income is significantly more attractive than it was at the start of 2022, when the yield to maturity of the Index was around 1.7%.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

Fixed interest | -0.8 | 3.7 | 2.2 |

The Cash benchmark was the best performing asset class over the June quarter as the Bloomberg AusBond Bank Bill Index delivered 1.1%.

At both Board meetings during the quarter, the RBA maintained its official cash rate at 4.35%. The slower decline in inflation than anticipated has adjusted the risks around inflation resulting in the RBA Board reopening discussions around the possibility of a rate hike in the May meeting before ultimately resolving to hold rates steady.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

| Cash | 1.1 | 4.4 | 1.9 |

The chart below compares one and ten year returns for the major asset classes, as at 30 June 2024.