We use cookies to improve your experience on our website. By continuing you acknowledge cookies are being used.

Investment market review - Quarter ended 31 December 2025

- Title

- Investment market review - Quarter ended 31 December 2025

The Research Team provides a performance summary and commentary on each of the five main asset classes.

Australian shares

Australian Equities eased by -0.9% underperforming global markets in the 4th quarter of 2025 as the tone of the Reserve Bank of Australian (RBA) after stronger than expected inflation and employment data throughout October and November put any further interest rate easing in doubt. As a result of this strong than expected data, longer term bond yields rose putting pressure on equity valuations on growth sectors such as Information technology, Health Care and interest rate sensitive sectors such as Consumer Discretionary and Financials.

The Material sector is the standout sector for the quarter (13.0%) and year (36%) supported by strong gold and copper prices (year on year increase of 146% and 39% respectively). Strong Copper prices offset stagnant Iron ore prices (-2% y.o.y.) helping our biggest minders BHP (15%) and Rio Tinto (25%) deliver strong returns for the 2025. Australian Smaller Companies outperformed their global counterparts, topping off a strong year. Smaller Material companies, especially gold explorers and producers assisted performance, Other small cap companies benefited from the strong Australian economy and labour market combined with the relatively attractive starting valuations.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

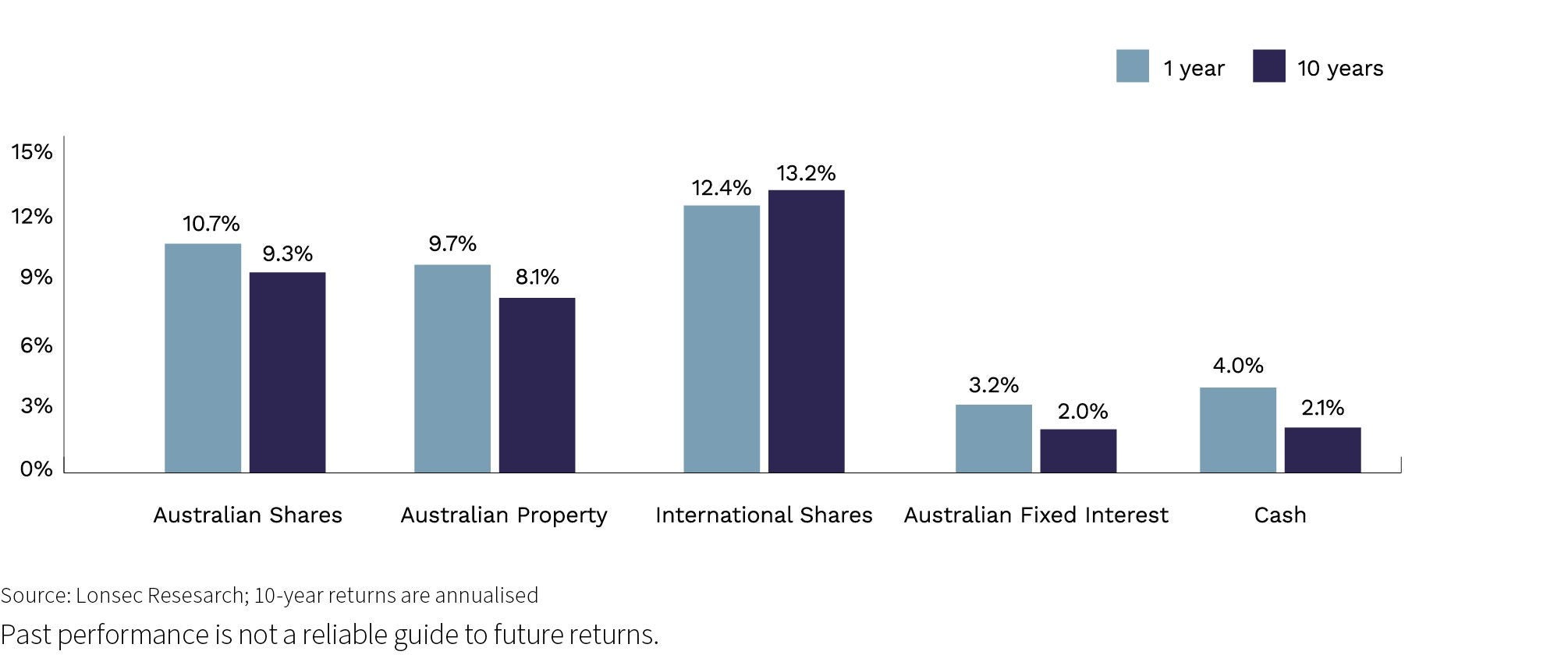

| Australian shares | -0.9 | 10.7 | 9.3 |

Australian listed property trusts

Over the quarter long-term bond yields rose putting pressure on the capitalisation rates of Listed Property trusts generally, but the performance of the largest index holdings Goodman Group was also a drag on performance. Goodman Group and its exposure to the data centre development, had resulted in high valuations and lofty expectations, so when it reaffirmed its existing growth guidance for its September 2026 quarterly guidance investors took profits. Goodman Group declined 12.3% over the year but has delivered 22.6% per annum compound returns over the past 3 years.

Global REITs were also impacted by rising global bond rates over the quarter with the hedged index delivering easing 1.4%.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

| Australian listed property trusts | -1.2 | 9.7 | 8.1 |

International shares

Global equity markets delivered strong positive returns over the quarter helping to drive positive double digit returns over a volatile 2025.

The US stock market continued to benefit from AI and Technology strength as well as a 0.25% easing in interest rates by the US Federal Reserve in December. South Korea and Taiwan equity markets also benefited from semiconductor and technology stock strength.

While technology remained a strong sector, performance also broadened out to other areas including global Financials, Health Care and Industrials. The market also saw European and Asian equities outperform the US market over the quarter and 2025.

The Australian dollar (AUD) rose against all currencies over the quarter, supported by rising bond yields and strong commodity prices. The AUD was also strong against the US dollar and Japanese Yen over 2025 reducing returns for Australian investors. The Euro has strengthened against all currencies over 2025 lifting returns from European equities for Australian investors and partially offsetting the headwinds created by the US dollar and Yen.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

International shares | 2.5 | 12.4 | 13.2 |

Fixed interest

Bond markets faced pressure in during the final quarter of 2025. Australian bond yields rose as November’s inflation figures remained above the RBA’s target band.

The RBA held interest rates steady over the quarter but revised its inflation forecasts significantly higher – the trimmed mean forecast for June 2026 was adjusted from 2.6% to 3.2% or from within the RBA’s target band of 2-3% to above the target.

This adjusted outlook changed expectations for the path of interest rates over the short and medium term. The longer-term bond yields rose to reflect this expectation. The 3-year bond yield unwound the expectation of further near-term cuts and began to factor in a higher level of “neutral” interest rates - the interest rate setting balanced between being stimulating or restrictive.

The rise in longer term bond years resulted in the capital value of the bonds declining and delivering negative returns over the quarter. However, this does mean that the running yield on Australian Bonds is now higher than in September providing more income per dollar invested.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

Fixed interest | -1.2 | 3.2 | 2.0 |

Cash

The official RBA cash level was 3.6% on 31 December.

After early 2025 saw several interest rate cuts, monetary policy momentum reversed in the final quarter as persistent inflation data forced the Reserve Bank of Australia (RBA) to take a more restrictive tone as it reduced expectations of further interest rate cuts over the near term.

The next move by the RBA in 2026 is now less certain as economic data reflects resilient private demand, a continued strong labour market and inflation stubbornly above the RBAs target. There is a growing expectation that should these factors continue to remain strong, the RBA may even have to increase interest rates at some point in 2026.

| 3-month return (%) | 1 year (% p.a.) | 10 year (% p.a.) |

|---|---|---|---|

| Cash | 0.9 | 4.0 | 2.1 |

Historical one and ten year returns

The chart below compares one and ten year returns for the major asset classes, as at 31 December 2025.

Seek advice

A qualified financial adviser can help you make sense of your options and ensure your super and investments are structured appropriately. Contact us for a complimentary discussion to see if advice is right for you.